8.9% of Profits Finally Enter the Buy Zone From Annaly Capital (NLY.PR.I)

")

Annaly Capital Management (NLY) has 4 preferred stocks. I have traded them from time to time. For now, what I’m happy with is NLY-I (NLY.PR.I).

I have written about NLY-I shares several times. However, it was rare that we were able to post bullish ratings on them. Usually stocks are good slightly above which we intend to enter the REIT Forum. That means they are usually about 0.2% to 1.5% above our targets. Our targets adjust for dividend accrual, so they continue to increase until the ex-dividend date, then decrease with the share price.

Chance strikes

Recently, we have seen a little weakness in NLY-I shares. The weakness allows us to exit with a bullish estimate. Currently, NLY-I shares are trading at $25.01. That gives them an annualized yield of about 4.7%. That sounds very sad. However, investors should be aware that a low call yield can only occur if the shares are called quickly. If there is a delay before the call occurs, then investors will be collecting a yield of about 8.94% during that time. That is very attractive.

Annaly Capital Management would have called

Annaly Capital Management has had many opportunities to drive these stocks already. They first called and floated on June 30, 2024. We’re almost 21 months past the date the shares first hit.

In addition, NLY-F (NLY.PR.F) shares are also floating rate shares with similar distributions. Those shares started floating on 30 September 2022. NLY-F has not been called despite being floated for more than 3 years.

Relative Value

I believe NLY-I is more attractive than NLY-F because NLY-I costs 36 cents less ($25.01 vs. $25.37) and the yield is better.

REIT platform

The dividend policy results in NLY-I having slightly larger dividends. At first glance, it may appear that NLY-F will have slightly larger dividends because the floating spread is 1.4 basis points higher (basically rounding error). However, NLY-I uses a favorable method of calculating benefits. It uses the actual number of days in the division period divided into a 360-day year. That sounds complicated, but I’ll make it simple.

- Take 365 days of accumulation and divide by 360 days (the official number of days).

- You get 1.0138889.

- Rounded it to 101.4% because I don’t want to type that many numbers again.

- Therefore, NLY-I receives approximately 101.4% of the expected cumulative profit each year.

As a result, our NLY-I targets are slightly higher than our NLY-F targets. However, the market was valuing NLY-F at a higher price than NLY-I. As a result, the annual yield of the NLY-F call is negative, but the annual yield of the NLY-I call is positive. Not great, but okay. Remember that you only get such a small yield if the shares are called soon after you buy them. The longer the shares remain outstanding, the better the yield. If they are not called at all, then you have a yield of around 8.95% with quarterly payments. That is very good.

Since shares can be called on 30 days’ notice, we arrive at our annual return estimate using that shorter 30-day window. Getting stuck with returns of 3% to 5% per month is not bad. But if you get less than 3%, then you really want it to be short term. This is surprising because, all else being equal, you generally want call protection to be there.

You won’t get call protection on shares that are already floating, however. Floating-rate stocks in this industry were originally fixed-rate stocks that switched to floating rate at the same time that stocks began to crash. Because treasury rates have soared in the past few years, floating-rate stocks are more attractive.

Beware of NLY-G

NLY-G almost always exceeds our targets. I chastise it for having such a thin floating spread. The market doesn’t seem to have a problem, but I see it as a big problem because it makes NLY-G even more dependent on short-term interest rates.

Target Setup

One of my goals in setting the NLY-Mina goals was that they would lead to very little reward calling. Today we have a good call yield and a slight discount to our target prices. Therefore, I approach stocks with the mindset of collecting attractive yields until we see a price drop. I believe we will probably see a modest increase in the stripped price at some point. That means the share price prepared to collect dividends it is likely to increase by 0.5% to 1.5%. So the objective is to collect the dividend yield for now and eventually collect a modest price improvement.

If we see the issued price go up by about 1% or 1.5%, that would be a signal to me that it will be time to consider taking the gains and looking at redistributing. These are solid stocks, though. If market tips are low, they probably won’t fall as much. If so, I can end up working well but working hard. That will still be fine, because it will allow us to re-share positive ratings. Don’t let the perfect be the enemy of the good.

Of course, it is always possible that the price of shares can go down further. However, historically, we have never seen that much. Since NLY started floating, it rarely trades below $25. That makes sense for several reasons. The first is that it leads to a return of around 9% or more when the Fed funds rate is high. The bottom line is that there are many buyers of stocks around $25 because there are many retail investors who can scan high-yielding stocks and sell below $25. That creates a decent level of support for the shares and explains why they have largely refused to go below $25 without a big hit in the markets around Independence Day.

Looking for an Alpha

For Juniors in Financial Management Annaly

Annaly Capital Management is a mortgage REIT. They have a number of mortgage backed securities. Most of the portfolio is in mortgage-backed agency stocks. Those have strong credit qualities because they are backed by Fannie Mae and Freddie Mac. As a result, mortgage REITs that focus on agency loans, such as Annaly Capital Management, Dynex Capital, and AGNC Investment Corp., typically have a lower level of risk for their preferred stocks. Some investors absolutely love the business model of agency mortgage REITs. They see huge profits in common stocks and significant “earnings”, making the stocks look very cheap for high earnings.

However, many of those investors do not understand how the income metric for mortgage REITs works. They may be confused with how dividends are calculated based on historical value and how hedges flow through the income statement. As a result, for most investors, it is best to focus on preferred stocks. We cover common stocks within our service. However, for now, the REIT platform finds NLY-I more attractive than common stocks.

Senior Position

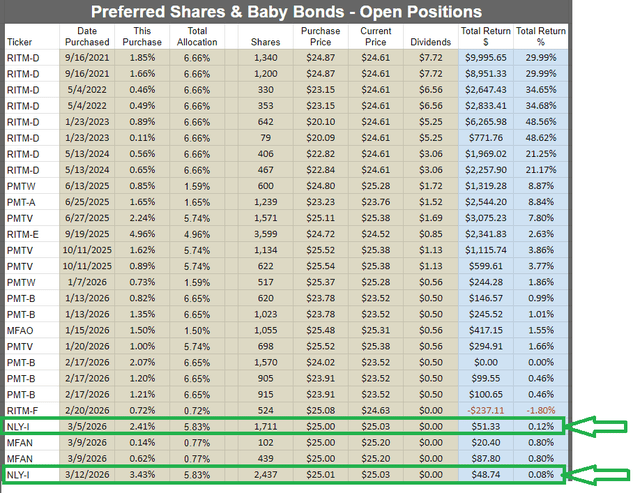

I have been buying NLY-I recently. This screenshot is from our subscriber tool showing all of our open positions. We separate preferred stocks and junior bonds into other categories, so this shows only preferred stocks and junior bonds:

REIT platform

It cuts off before showing the new positions we added on 3/16/2026, but I think that’s a large number of open trades for an analyst to include in their headline.

The conclusion

NLY-I offers an attractive combination of stable valuation and strong dividend yield. Although it could go down further, I find it unlikely. I expect minor resistance around $25.00, as seen in the testing tools for more investors if it gets to that price or a few pennies below.

Therefore, I believe that the downside is low while the yield is high. We have the potential for a modest increase in the share price, but I would only expect about 1% to 1.5% in excess of retained earnings. Since dividend accrual works out to about 9%, that’s not too bad.

I put over $100k into getting 4,148 shares of NLY-I. I eat my cooking. Right now, it tastes like 9% with a little high.

We do not measure NLY’s standard shares in this article.